When you pick up a prescription at the pharmacy, you might not think about why your generic pill costs $10 while the brand-name version costs $75. But behind that price difference is a complex system designed by your employer’s health plan-and it’s not always working in your favor.

Why Your Plan Pushes Generic Drugs

Your employer’s health plan doesn’t just prefer generic drugs-it actively pushes them. Why? Because generics are 80-85% cheaper than brand-name drugs. The FDA confirms they’re just as safe and effective. The difference isn’t in quality-it’s in cost. Brand-name makers spend millions on advertising, clinical trials, and marketing. Generic manufacturers skip all that. They just copy the active ingredient and sell it for a fraction of the price.That’s why 99% of large employer health plans include prescription drug coverage, and nearly all of them put generics in the lowest cost tier. In most plans, Tier 1 is for generics. That means you pay $10 or less. Tier 2 might be preferred brand-name drugs-maybe $40. Tier 3 is non-preferred brands-$75 or more. And Tier 4? That’s for specialty drugs, often costing hundreds per month.

When a brand-name drug goes generic, the system automatically shifts. The new generic lands in Tier 1. The old brand name gets kicked to Tier 4. If you keep taking the brand, your out-of-pocket cost jumps from $40 to $75-or worse. It’s not a coincidence. It’s designed that way.

How Formularies Work (And Why They Change Without Warning)

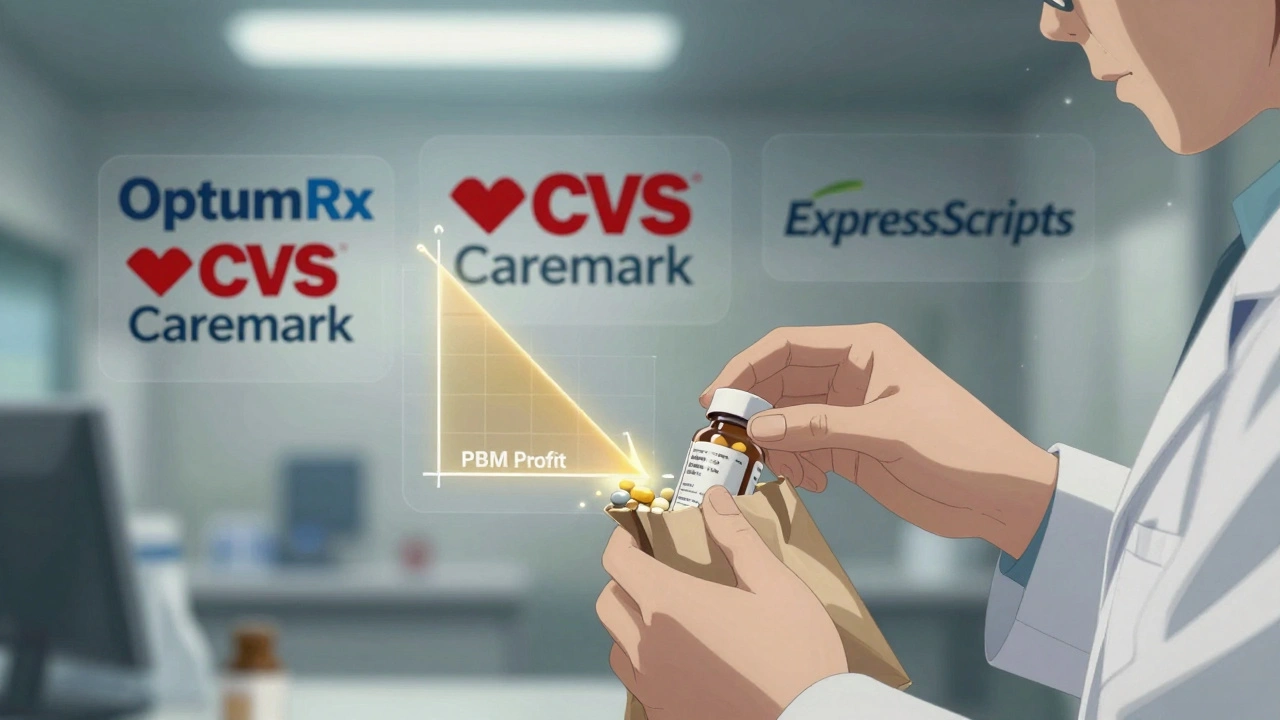

Your plan’s formulary is a list of drugs it covers-and how much you pay for each. It’s not fixed. It changes constantly. The Ohio Department of Administrative Services says these changes can happen anytime, with no advance notice. That’s because Pharmacy Benefit Managers (PBMs)-like OptumRx, CVS Caremark, and Express Scripts-control the list.PBMs don’t just manage claims. They negotiate with drug makers. And their biggest tool? Exclusion. In January 2024, each of the three biggest PBMs removed over 600 drugs from their formularies. That’s more than 1,800 drugs pulled nationwide in one month. Why? To pressure drug companies into offering bigger discounts. If a company won’t give a good rebate, the drug gets dropped.

Here’s the catch: you might not know your medication was removed until you show up at the pharmacy and it’s denied. You might be on a stable medication for diabetes, high blood pressure, or asthma-and suddenly, your plan won’t cover it anymore. You’re left with two options: pay full price, or ask for a medical exception. Neither is easy.

The Hidden Gap: Why You Don’t See the Savings

You’ve heard that generics save $3 billion a week. That’s true. But here’s what no one tells you: those savings don’t always reach you.PBMs use something called gross-to-net pricing. A drug’s list price might be $100. But after rebates, discounts, and returns, the PBM pays $45. That 55% difference? That’s the GTN spread. The drug company pays the PBM a rebate to keep the drug on the formulary. The PBM keeps part of that rebate. You never see it.

So even though your plan saves money by switching you to a generic, your copay stays the same. The savings go to the PBM and your employer-not to your wallet. Some employers pass savings along in lower premiums. Others don’t. You’re left wondering why your drug costs didn’t drop, even though the system claims to be saving money.

What You Can Do to Protect Yourself

You can’t control your plan’s formulary. But you can control how you respond to it.- Check your formulary every time you refill. Don’t assume your drug is still covered. Visit your insurer’s website or call them directly. Look for the “Drug List” or “Formulary” section in your Summary of Benefits and Coverage.

- Ask if a generic is available. Even if your doctor prescribed a brand name, ask if a generic version exists. Many drugs have generics you didn’t know about.

- Use in-network pharmacies. Some plans, like HealthOptions.org’s Price Assure Program, automatically lower your cost for generics at in-network pharmacies. Out-of-network? You could pay double.

- Request a formulary exception. If your drug was removed or moved to a high tier, your doctor can file an exception. You’ll need to prove medical necessity-like if the generic didn’t work or caused side effects.

- Use care management programs. Many employer plans offer care managers who help you find affordable alternatives. Call your insurer and ask if one is available.

When Your Employer Uses a CDHP

Consumer-Driven Health Plans (CDHPs) are growing fast. These plans combine high deductibles with health savings accounts (HSAs). They’re designed to make you more price-conscious.That sounds good-until you realize your HSA contributions might not cover your drug costs. If you’re on a chronic condition like diabetes or COPD, your monthly drug bill could be $300 or more. Even with a generic, you might pay $75 per month. That’s $900 a year. Your HSA might not keep up.

Employers using CDHPs often push generics harder because they’re the only way to make the math work. But they also need to educate employees. Schauer Group found that many people are willing to use generics-they just don’t know enough to feel comfortable. Your employer should be giving you clear info: emails, payroll inserts, videos, even text alerts when your drug changes tiers.

If they’re not, ask. Demand it. You’re paying for this benefit. You deserve to understand how it works.

The Bigger Picture: Who Really Controls Your Medicine?

Your employer picks the plan. But the PBM writes the rules. And the drug maker writes the price. You’re caught in the middle.Three PBMs control most employer plans. They decide which drugs are covered, which aren’t, and how much you pay. They use exclusions as leverage to force drug makers into deeper discounts. But you’re the one who loses access when a drug disappears from the list.

There’s no easy fix. But awareness helps. The more you understand how formularies work, the less likely you are to be blindsided. You’ll know to check your coverage before your refill. You’ll know to ask for alternatives. You’ll know to push back when your drug is pulled.

Generic drugs aren’t the enemy. They’re the solution. But the system around them is broken. It saves money-but not always for you. The real challenge isn’t finding cheaper drugs. It’s making sure the savings reach the people who need them most.

Why is my generic drug suddenly more expensive?

Your plan’s formulary may have changed. Even if the drug is still generic, your insurer could have moved it to a higher tier, or your pharmacy could now be out-of-network. Check your insurer’s website for updates or call their customer service. Changes happen often, and without notice.

Can I still get my brand-name drug if it’s not on the formulary?

Yes, but you’ll pay full price unless your doctor files a medical exception. This requires documentation showing the generic didn’t work, caused side effects, or isn’t appropriate for your condition. Approval isn’t guaranteed, but it’s your only path if you need the brand.

Do all employer plans have the same formulary tiers?

No. While most use a 4-tier system (generic, preferred brand, non-preferred brand, specialty), the exact copays and drug lists vary. Anthem, for example, uses six different formulary types depending on the employer plan. Always check your specific plan’s details.

Why do PBMs remove drugs from formularies?

PBMs remove drugs to pressure manufacturers into offering bigger rebates. If a drug maker refuses to lower the net price, the PBM drops it from the list. This is a negotiation tactic-and it’s becoming more common. Over 1,800 drugs were removed by the top three PBMs in January 2024 alone.

Are generic drugs really as good as brand-name ones?

Yes. The FDA requires generics to have the same active ingredient, strength, dosage form, and route of administration as the brand. They must also meet the same quality and safety standards. The only differences are in inactive ingredients, packaging, or price-never effectiveness.

What should I do if my medication was removed from the formulary?

First, ask your pharmacist if there’s a generic or alternative on the formulary. Then, contact your doctor to discuss options. If no alternatives work, ask your doctor to file a formulary exception with your insurer. You can also reach out to your employer’s HR or benefits team-they may have a care manager who can help.

How can I find out what drugs my plan covers?

Log in to your insurer’s member portal and look for the “Drug List,” “Formulary,” or “Prescription Coverage” section. You can also call customer service or request a printed copy of your Summary of Benefits and Coverage (SBC). Don’t rely on memory-formularies change often.

Comments

Nancy Carlsen

I just found out my generic blood pressure med got moved to Tier 3 last month 😭 I had no idea until I got to the pharmacy. Thank you for explaining why this happens - now I know to check my formulary every time I refill. 🙏❤️

Kurt Russell

THIS. IS. A. SCAM. 🤯 PBMs are sucking the life out of regular people while pretending they’re saving us money. I’ve been on the same med for 7 years - suddenly it’s $120 a month because some corporate suit decided to ‘negotiate.’ My wallet’s crying. Someone needs to burn this whole system down.

Kyle Flores

i didnt even know what a pbm was until last year. now i check my drug list like its my daily horoscope. its wild how much power these companies have and how little we’re told. my grandma got switched to a generic that gave her migraines - took 3 months and 2 appeals to get her old one back. dont wait till it’s too late. check your stuff.

Ryan Sullivan

The structural inefficiencies inherent in the PBM-gross-to-net pricing model are a textbook example of misaligned incentives. The agency problem between fiduciary duty and profit maximization is exacerbated by opacity in rebate structures. It’s not merely a pricing issue - it’s a governance failure.

Wesley Phillips

so like… the system is literally rigged and we’re the pawns? wow. thanks for the detailed breakdown. now i feel like i need a degree in pharmacy law just to buy ibuprofen. 🤦♂️

Olivia Hand

I’ve been quietly documenting every formulary change for my dad’s diabetes meds. 14 changes in 18 months. Every time I call customer service, they say ‘it’s a network issue’ or ‘we’re updating.’ No one takes responsibility. It’s exhausting.

Desmond Khoo

i switched to generics years ago and thought i was being smart. turns out i was just funding someone else’s bonus. but hey - at least i’m not paying $200 for a pill that does the same thing. still feels shady tho 🤷♂️

Ernie Blevins

People complain about drug prices but never take responsibility. If you’re on a chronic med, you should be doing your own research. This isn’t hard. Stop blaming the system and start being proactive.

Ted Rosenwasser

I’ve read the FDA’s bioequivalence guidelines. Generics are statistically indistinguishable in efficacy. Anyone who still thinks brand-name is better is either misinformed or being paid by Big Pharma. Wake up.

Ashley Farmer

My sister had to switch to a new generic for her anxiety med last year. It made her feel like a zombie. She was terrified to speak up because she didn’t want to be ‘difficult.’ I’m so glad you mentioned medical exceptions - she finally asked, and they approved the old one. Thank you for giving people permission to fight.

Jennifer Anderson

i just checked my formulary and my med is still there phew. but i have no idea if it’ll be next month. i just hope they send a text or something before i get to the pharmacy with my heart in my throat 😅

Sadie Nastor

i used to think generics were just cheaper versions. now i know they’re bargaining chips. still taking mine - but now i’m keeping receipts, screenshots, and calling HR every time something changes. small wins, right? 💛